By Shawna Bertalot, CIC, ACI, WisMed Assure President

The WisMed Assure team spends a lot of time the first half of the year doing Medical Student and Resident education on topics especially important to those who are completing their education and heading off to their first jobs. Part of that education is Medical Professional Liability (Med Mal) 101. While most physicians are now employed by large groups, hospitals or health systems that purchase their Med Mal insurance for them, there are a few key elements and responsibilities that every physician should know.

Med Mal insurance requirements vary by state. Wisconsin has strong tort reform laws* and requires all physicians and CRNAs who are licensed and practice in the state to carry insurance limits of $1M per medical incident and $3M aggregate per policy year. This insurance must be with an insurance carrier approved by the Wisconsin Office of Commissioner of Insurance to qualify for the unlimited excess coverage of the Injured Patients and Families Compensation Fund (IPFCF). Illinois by comparison has no requirement for physicians to carry insurance, no excess liability fund and no tort reform, thus insurance premiums and severity of claim awards are much higher than in Wisconsin.

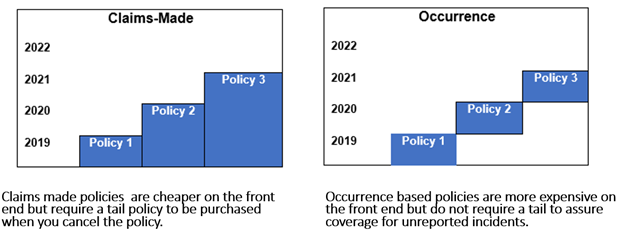

It is important for you to know and track the type of Med Mal policy you have throughout your career. The two types are Claims-Made and Occurrence; the primary difference being whether the policy covers claims that are MADE during the policy year or claims where the alleged wrongful event OCCURRED during the policy year.

The most important difference is that if you have a Claims-Made policy and you leave your employer or cancel the policy, all coverage ends unless an “Extended Reported Period,” commonly called “Tail” coverage, is purchased. If you are employed, you need to know if your policy is Claims-Made and who is responsible for purchasing a Tail per your contract. If your employer requires you to pay for the tail upon leaving, then it would be beneficial to check with your employer’s risk manager, insurance agent, or company to determine the cost. The IPFCF requires that a tail is purchased.

Understanding your responsibilities under the IPFCF is an important responsibility that rests with each individual physician. In January 2023, the IPFCF implemented a new policy and administration system that allows participants to review their status and pay online. Your employer may handle the primary insurance and payment of IFPCF fees; however, it is the responsibility of every resident and physician to know their status and maintain compliance with the IPFCF. Click here for more information.

We recommend all physicians keep their own file on their Med Mal coverage. This file should include a Certificate of Insurance for each year of coverage. This certificate will show your policy number, insurance carrier information, and limits of coverage. Generally, Medical Staffing and Credentialing offices can provide you with copies of your insurance information. You should also keep a file on any claims including dates and final resolution. This will allow for a much smoother credentialing and on-boarding experience.

Wisconsin is a great state to practice medicine, especially for physicians. As discussed above, the IPFCF and the state law that established it, Wis. Statute Chapter 655, create certain responsibilities to carry Med Mal insurance and pay annual IPFCF fees. That said, Statute 655 and the tort reform that the Wisconsin Medical Society advocates for and works hard every year to protect make Wisconsin one of the best judicial environments with the lowest Med Mal premium rates. Only eight states have some sort of excess patient compensation fund for Med Mal, and Wisconsin is the only state to provide unlimited coverage beyond the required $1M primary Med Mal insurance.

Please contact your WisMed Assure agent or shawna.bertalot@wismedasure.org with any questions.

*Thirty-three states have imposed caps on damages sustained in Med Mal lawsuits. The caps range from $250,000 per incident to as much as $2.25 million. In Wisconsin, non-economic damages are capped at $750,000.

Note: This article is for informational purposes only and should not be considered as insurance advice related to your specific policy or situation. Please consult with a qualified insurance advisor or professional before making any policy decisions. Full disclaimer and contact information.