Injured Patients and Families Compensation Fund Announces Premium Holiday

On Wednesday, June 17, 2020, the Injured Patients and Families Compensation Fund (fund) approved waiving the upcoming fiscal year’s premiums for physicians, CRNAs and hospitals enrolled in the fund.

The Society has been working hard to find ways to assist its membership during these unprecedented times. The premium holiday was originally requested by the Society and endorsed by the fund’s Actuarial and Underwriting and Finance/Investment/Audit committees before it was approved by the Board. The premium holiday will be in effect from July 1, 2020 through June 30, 2021. Read More

MPL Market + COVID-19 = What Next?

The COVID-19 crisis will add pressure to an already “stressed out” underwriting environment.

Carriers are now responding to demands of COVID-19 with premium relief and underwriting flexibility (e.g. waiving requests for supplemental information on telemedicine or cross-state boarder practice). This lowers their premium base and handicaps underwriting.“In this environment, I’ve never been more acutely aware of our mission at the Wisconsin Medical Society and WisMed Assure and I am proud of how we and our community of physicians have responded,” says Shawna Bertalot, WisMed Assure President. Read More

Shawna Bertalot is the president of the WisMed Assure agency. With her strong leadership skills and knowledge of the industry, our skilled team of agents are motivated and well prepared to find solutions for our clients.

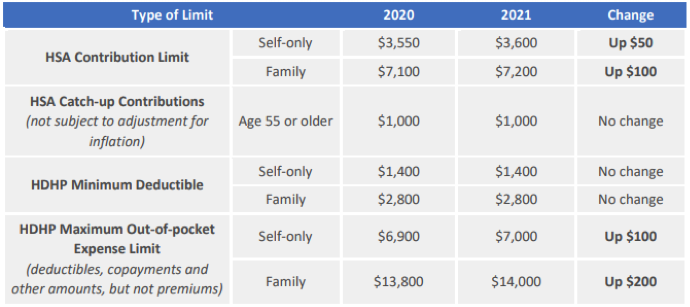

Navigating Testing in a COVID Environment

By Chris Noffke, GBDS – VP of Employee Benefits

Navigating insurance benefits is complex and confusing for consumers and business owners alike. People seeking benefits are expected to understand insurance terms like deductibles, coinsurance, out of pocket limits, annual out of pocket limits (yes this can have a different maximum risk amount) and many others.

On top of that, you now have to understand the ins and outs of preventative care coverages and COVID related no-cost, shared-cost coverages. Read More

Announcement

Chris Noffke: Vice President, Employee Benefits

I am pleased to announce the promotion of Chris Noffke from Director of Group Benefits to Vice President, Employee Benefits. Chris has been with WisMed Assure for four years and has worked as an insurance advisor for more than 15 years.

In his role as vice president, Chris will focus on advancing WisMed Assure’s ability to deliver superior employee benefit solutions and service to an ever-growing number of healthcare providers.

Chris has already played a key role in the creation of several important initiatives and programs including the association health plan, a pooled disability program, and the improvement of the pricing and value of our dental program. He is currently working on the development of a national medical cooperative and a national association health plan.

Prior to joining WisMed Assure, Chris held positions at WPS, EPIC Life, Group Health Cooperative of South-Central Wisconsin and Ameritas Group, as well as operating his own insurance agency. He has completed the National Association of Health Underwriters Voluntary/Worksite Certification and holds a Group Benefit Disability Specialist (GBDS) designation and is studying to become a Certified Self-Funding Specialist (CSFS).

Chris has a Bachelor of Arts degree from the University of Nebraska.

On behalf of the entire WisMed Assure team, I congratulate Chris on reaching this important milestone and look forward to supporting his continued success.

Shawna Bertalot, CIC, ACI, President

We’re growing!

Insurance Advisor joins the WisMed team

At WisMed Assure, we are always looking for and developing new and better ways to serve the Wisconsin medical community. This includes developing our team of dedicated professionals through education, training, and, when needed, hiring proven expertise.

We are delighted to announce Tom Strangstalien has joined our team to bolster our financial services capabilities. Tom specializes in individual financial protection including life, disability and long-term care insurance.

Tom has over 25 years of experience in the financial-protection business. He believes clients should be treated in the same way he and his family would like to be treated and that building relationships is crucial to delivering the best possible service and value.

Tom attended Viterbo University, majoring in Business Administration and Finance, graduating with honors, Magna Cum Laude. Throughout his career, Tom has earned numerous awards and recognition, including top of the table at several insurance companies, and becoming a member of the Million Dollar Round Table.

When Tom is not busy protecting the financial wellbeing of his clients, he enjoys traveling and seeking out new experiences with his wife and their four children. On any given weekend, you can find Tom, fishing, hunting, or hiking and creating memories that will become tall fish tales, some even true.

We are excited to welcome Tom to the WisMed Assure team and look forward to working with him to assure our clients’ financial health and security.

Wisconsin Medical Society Declares Racism to be a Public Health Crisis

Racism is a constant threat to health, medical care and longevity in America. The Wisconsin Medical Society, driven by its mission to improve the health of the people of Wisconsin, declares racism to be a Public Health Crisis and calls for equity in health.

Racism threatens health. Racism worsens the social determinants of health, including housing, employment, education, community and neighborhood, food and medical care. Poor housing, including homelessness, results in illnesses such as diabetes and asthma. Unemployment increases heart disease risks and overall mortality; poor education increases death from diabetes; physical space loss for exercise increases childhood obesity; and food deserts significantly increase African-American obesity. The greatest health threat faced today in COVID-19 has further revealed these profound disparities demonstrated by the disproportionate mortality in communities of color.

The human toll is destructive and untenable. To move forward, we must take a stand against racism. In doing so, we stand in solidarity with organizations across the state and our country condemning racism, injustice, and health disparities.

The Society, along with many other healthcare organizations, is taking a strong stand and has identified seven key recommendations for change. You can learn more here.

Different Kinds of Debt: The Good, the Bad, and the Just-Don’t-Do-It!

By Rufus Sweeney

Amassing a considerable amount of debt during medical school is “situation normal” for practically every medical student. Even though debt is rarely seen as a good thing, you need to know the difference between good debt, bad debt, and debt to be avoided at all cost.

Choosing wisely now makes paying off your debt much easier. Read More